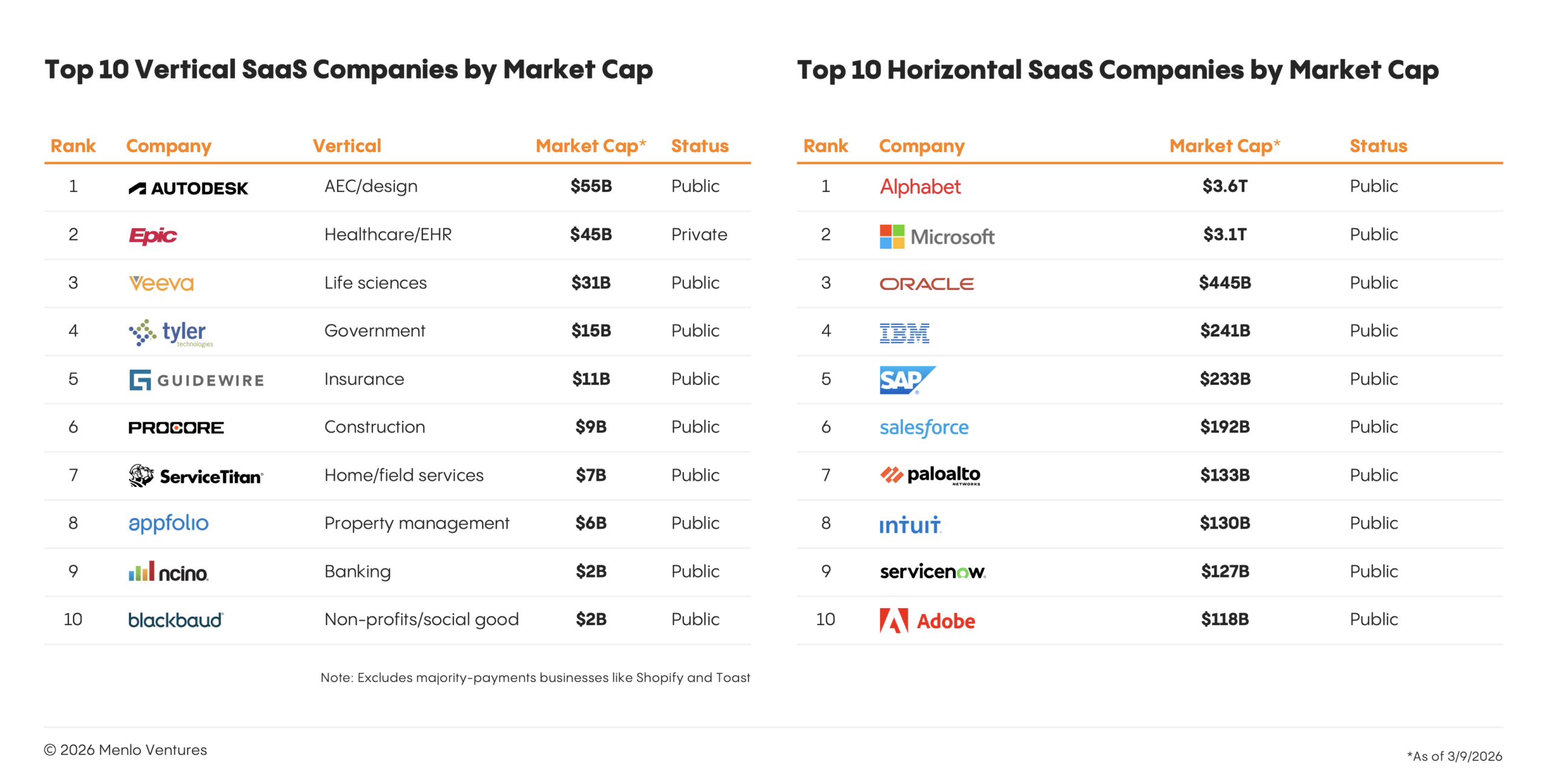

Vertical software has always punched below its weight. For all the defensibility that Epic, Veeva, and Procore built, the category never escaped a persistent ceiling—it competed for IT budgets, required new headcount to manage, and sat alongside the work rather than inside it—all within a bounded customer base. The market cap distribution tells the story: While roughly 30 horizontal SaaS companies trade above $10 billion, only seven vertical SaaS companies do, and of these, Shopify and Toast get the majority of their value through payments, not software. The TAM critique that followed vertical SaaS for two decades (markets too small, expansion too hard) was a symptom of this limitation.

We believe vertical AI, however, breaks that ceiling. Understanding why requires unpacking not just what changed technically, but what it means structurally for the businesses being built on top of it.

There is a lively discourse around AI’s impact on software right now—scenario analyses, moat taxonomies, bear cases for SaaS broadly. We find most of it more useful as a set of stress tests than as a guide to where value actually accrues. The more important question for founders is not whether AI disrupts vertical software, but what it takes to build something lasting in this specific moment.

Vertical SaaS Set the Stage…and Hit a Ceiling

Vertical SaaS was the first true digitization layer built for specific industries. Before it, workflows lived in a patchwork of horizontal tools, institutional knowledge walked out the door when people left, and compliance was largely manual. Vertical SaaS changed that by offering purpose-built systems of records and engagement that mirrored industry-specific workflows end to end.

The defensibility it built was real. System of record status, proprietary data models tuned to industry taxonomies, pre-built integrations, embedded workflows, and compliance logic baked directly into the product created switching costs that were structurally hard to replicate. The expertise required to build and maintain these platforms couldn’t credibly be replicated by a horizontal vendor bolting on an industry template, nor live in-house. Customers depended on the vendor.

But vertical SaaS hit a persistent ceiling. It competed for IT budgets rather than the far larger labor spend underneath it, and often required new headcount to manage. It sat alongside the work—a tool professionals went to, not something that participated in the work itself. The TAM critique leveled at vertical SaaS for years was a symptom of the fact that this software assisted and recorded, but didn’t do.

What Changes with Vertical AI

The shift from vertical SaaS to vertical AI is a change in what software fundamentally does: Vertical SaaS showed and assisted; vertical AI reasons and executes.

This moves the ROI calculation from software budgets to people budgets. Vertical businesses are fundamentally services organizations with labor as their dominant cost. In healthcare, administrative staff outnumber physicians, and $740 billion flows annually to administrative services against just $63 billion in IT. In higher education, administrative spending has grown 4x over 20 years to $240 billion, with some universities now having more administrators than students. In law, associate and paralegal time is both the core product and the largest expense on the P&L. In insurance, claims processing and underwriting are still overwhelmingly human workflows, with adjusters, reviewers, and call center staff handling each case individually. These industries didn’t underinvest in software because they were unsophisticated; they spent on labor because the work demanded judgment, context, and adaptability that prior generations of software couldn’t provide. That’s the gap vertical AI closes—not by digitizing a form, but by operating in real time, in context, at the point of decision.

Three capabilities distinguish vertical AI that enable them to perform the work vs. simply organize it: 1) compounding learning loops that improve with every interaction, 2) contextual reasoning that spans the full scope of a workflow, connecting variables that SaaS could store but never synthesize, and 3) concurrent execution of specialist-grade tasks. Together, these open up a category of businesses that the SaaS model structurally couldn’t support.

Finding Durability in Vertical AI

Think of the difference between a physician who’s completed their residency program versus a smart generalist you plan to train on the job. For some admin work, the generalist can be enough. But when the work requires real judgment (e.g., reading a complex case, knowing what matters) the physician’s built-in expertise is worth more than any amount of on-the-job training. Vertical AI works the same way: It enters the workflow with pre-loaded domain knowledge that a generalist model would have to acquire from scratch. Then every task and edge case handled makes the next decision better and makes the gap harder to close.

Not all vertical AI compounds this way. A tool confined to routine, rules-based tasks (e.g., status checks, appointment reminders, etc.) accumulates little domain-specific information that couldn’t be replicated rather quickly from scratch.

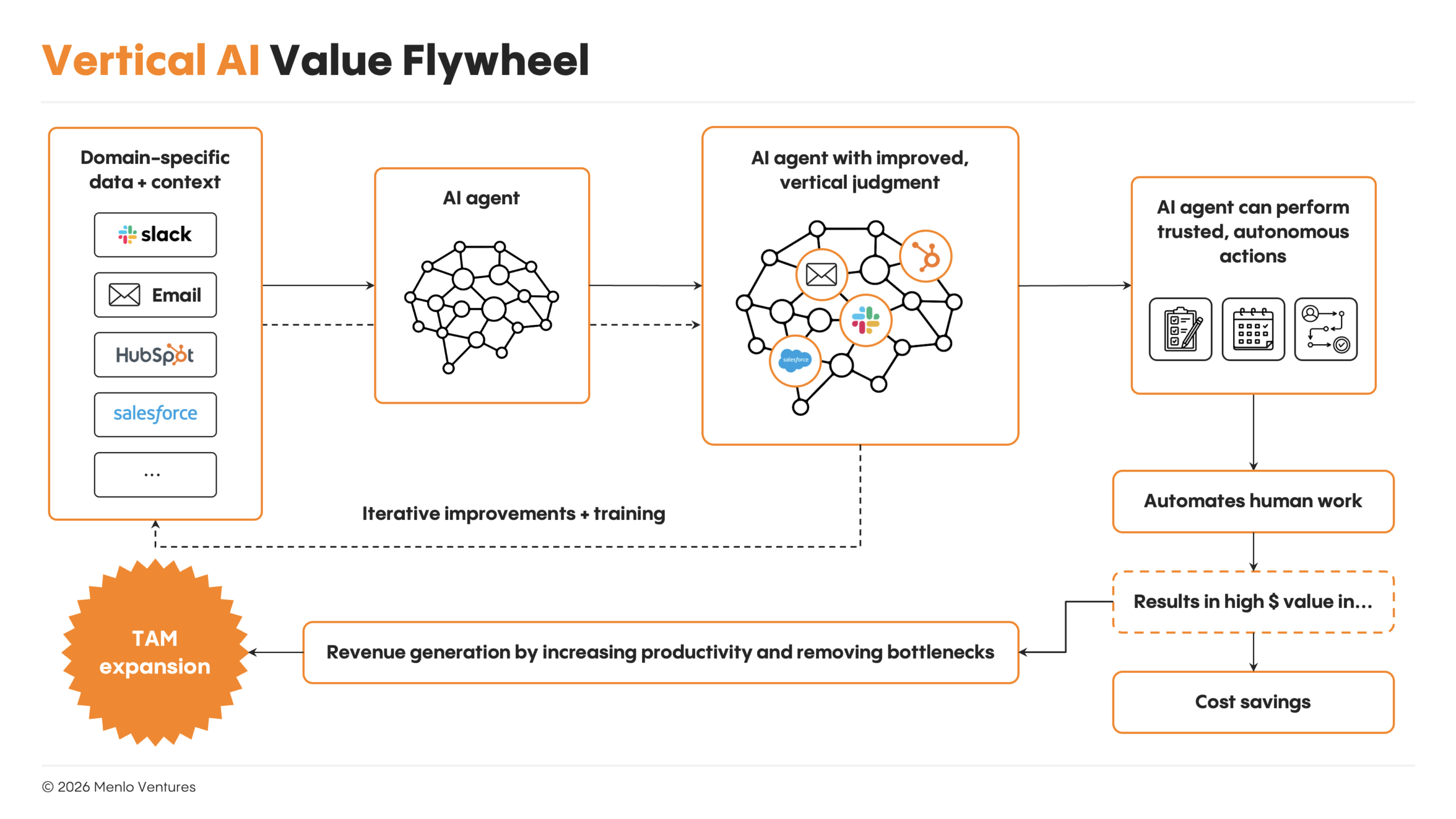

The most important structural insight about vertical AI is that its value compounds. The flywheel looks like this:

- An agent ingests domain-specific data and context;

- Develops judgment a general-purpose model can’t match;

- Earns trust to embed deeper into live workflows;

- Generates feedback and correction signals from real usage;

- Improves through that tuning, expands its scope of work—capturing more of the labor spend it competes against with each cycle.

It is also worth distinguishing between two types of moat that vertical AI companies can build. Defensive moats—regulatory certification, human sign-off requirements, compliance infrastructure—slow down competitors and set a floor on how quickly displacement can happen. Generative moats—compounding data, cross-customer signal, expanding workflow coverage—actively widen the gap over time. The most durable companies have both: The defensive moat buys time while the generative moat does its work. Companies with only one or neither tend to be the ones conceding ground at renewal.

A useful stress test for this is what we call the Clone Test: If you replicated the founding team and codebase today and gave the clone access to current frontier models, why wouldn’t it outcompete the original? For the companies we find most compelling, the answer is that the clone cannot quickly replicate what has been built—the data, the feedback and learnings through real-world task execution, and the network effects that have compounded on top of them. The four characteristics below are the conditions required to get this flywheel turning and keep it accelerating.

1. Go after labor, not IT budgets.

The most durable vertical AI companies measure ROI against the cost of the work itself—headcount, throughput, revenue recovered—rather than against a software line item. Grow Therapy* absorbs intake, scheduling, and insurance credentialing so clinicians can see more patients without adding staff. Legora* handles the research and drafting that would otherwise bill by the hour, so lawyers take on more clients without growing headcount. CollegeVine* deploys AI agents across university campuses to replace administrative workflows (e.g., enrollment, student services, transcript processing, etc.) so staff capacity compounds without proportionally hiring.

The companies competing for labor budgets get you into the work, which enables them to generate the usage, feedback, and correction signals that drive compounding improvement. On the contrary, companies competing for just IT budgets sit adjacent to the work with less opportunities to accumulate the same proprietary context.

2. Staying in the work.

The most durable vertical AI companies aren’t just automating a task; they’re embedded in the execution layer and staying in the work. The renewal cycle is where this distinction gets tested: As models improve and implementation knowledge diffuses, buyers arrive with credible alternatives—an internal build, a cheaper competitor, a newer point solution. Companies sitting alongside the work find their switching costs were lower than they appeared. Companies sitting inside it find the opposite: The data, the learned context, and the workflow integration make leaving structurally more expensive.

Naturally, companies operating at the point of decision are better protected. Pace, for example, handles the operational work of an insurance claim—reading documents across thousands of pages, applying carrier-specific business rules, and preparing claims files the way a BPO team would. Assort Health runs live patient calls across hundreds of providers, navigating specialty-specific scheduling and engagement protocols that took time to internalize. Rogo drafts memos, builds comps, and synthesizes deal precedents—the same work that junior bankers spend hours on. Because it’s doing the work, it accumulates institutional context with every engagement: how this firm structures analyses, what partners care about, which precedents matter. Replacing it means losing all of that and starting over.

A related model takes this even further. Rather than embedding inside a customer’s workflow, companies like Crosby, Gyde Health, and WithCoverage absorb the function entirely—a law firm in one case, and an insurance-broker relationship in the others. The buyer is purchasing an outcome, the budget line already exists, and the path into that spend is shorter from day one.

3. Compounding data moats.

The companies hardest to replicate are those whose products improve with usage in ways that are specific to their vertical and unavailable to general-purpose entrants. Not data at rest, but decision quality that compounds from interactions, codified judgment or taste, corrections, and edge cases accumulated over time. The strongest version of this is a product that sees across customers—building a signal from aggregated behavior that no single customer could construct alone and that a new entrant, by definition, cannot access on day one.

Eve* handles legal intake before a lawyer is involved, learning with every interaction which case characteristics predict successful outcomes and how to route work more accurately. NationGraph* maps government procedure opportunities across 100,000+ state, local, and education entities, growing more precise with every bid tracked. In doing so, Nationgraph learns which signals predict contract wins, which stakeholders matter, and how each agency’s process actually works. PermitFlow is accumulating a database of permits, jurisdictional rules, and approval workflows across thousands of municipalities, learning with every submission which documentation, sequencing, and regulatory nuances determine whether a permit clears or stalls. All of this becomes an increasingly precise map of how each jurisdiction actually operates.

4. Understanding the terrain.

Some have argued that technology tends to bulldoze existing landscapes rather than build on them. But in regulated verticals, a lot of what looks like inefficiency is actually structural. HIPAA compliance, FDA certification, and professional liability requirements don’t get easier to satisfy as models improve. Neither does earning the institutional trust required to operate inside clinical, legal, or financial workflows.

OpenEvidence* illustrates this well: Its network of verified clinicians and partnerships with leading medical journals enables a level of trust that can’t be replicated through any technological advancements. Solace* illustrates a different dimension: not just regulatory trust, but tacit operational knowledge. Solace has guided 200,000+ patients through Medicare coverage decisions, prior authorization appeals, and benefit navigation—learning which billing codes actually get reimbursed, which appeals arguments work with which payers, and how care coordinators route patients differently across systems.

Where the Next Wave Is

The verticals that produced the first generation of vertical AI leaders, healthcare and legal, share a few characteristics that are representative of what we look for in the next breakout verticals:

- High labor-to-IT spend ratio. The budget is in people, not software, which means AI that replaces work can capture meaningfully more value than AI that replaces tools.

- Manual, unstructured workflows. The work relies on judgment applied to messy inputs— documents, conversations, physical environments—rather than structured data entry. These are the workflows that prior generations of software couldn’t reach, but that multimodal AI now can.

- Regulatory or procedural complexity. Compliance requirements, licensing, fiduciary obligations, and jurisdiction-specific rules demand deep domain investment up front, which compounds into a durable moat that general-purpose entrants can’t shortcut.

- A forcing function. Labor shortages, margin pressure, or a regulatory shift creating urgency to act now rather than wait.

We see this profile across a number of markets today. A few examples include financial services adjacencies (e.g., accounting, wealth management, specialty insurance lines) that employ large back-office workforces performing high-judgment, repetitive tasks, and carry fiduciary obligations and regulatory reporting requirements that create friction. Construction, a $2.1 trillion industry dealing with labor shortages and razor-thin margins, is a clear example of unstructured workflows meeting new capability—multimodal AI makes previously unparseable physical-world documentation (site conditions, as-builts, RFIs) accessible for the first time, unlocking work that software simply couldn’t touch before. Home services is defined by its forcing function—PE-driven consolidation is creating the technical sophistication and ROI pressure necessary for AI adoption at the operator level, turning a large and largely untouched market into one with urgency to act.

The common thread across these markets is that the first wave of software often added as much overhead as it removed—new interfaces, new workflows, new headcount to manage the tools themselves. AI inverts that by making it possible to meet workers inside messy, real-world workflows rather than asking them to move into structured ones. And the complexity between where decisions are made and work gets done that limited vertical SaaS’s reach is precisely what creates the opening for AI.

If you’re building vertical AI where workflow, data, and judgment reinforce each other, we’d love to hear from you.

* Menlo Ventures portfolio company

Jean-Paul (JP) Sanday is a partner at Menlo Ventures who invests at the inflection stage. Focused on vertical SaaS and, more broadly, enterprise software, JP is particularly excited about companies defining the future of work, infusing our lives with intelligent automation and democratizing data analytics. His favorite part of the…

Croom is a partner at Menlo Ventures focused on financial technology, healthcare IT, and enterprise SaaS. Since joining Menlo in 2017, he led the firm’s Series A investment in Arch, Finch, Prodigal, and Rivet and has also invested in Fieldwire (acquired by Hilti), Fleetsmith (acquired by Apple), HOVER, Particle Health,…

As an investor at Menlo Ventures, Sam focuses on SaaS, AI/ML, and cloud infrastructure opportunities. She is passionate about supporting strong founders with a vision to transform an industry. Sam joined Menlo from the Boston Consulting Group, where she was a core member of the firm’s Principal Investors and Private…

Sabrina is an investor at Menlo Ventures, where she focuses on inflection-stage companies in enterprise SaaS, AI/ML, and cloud infrastructure. She’s excited about partnering with founders who challenge the status quo and supporting them in transforming bold visions into enduring businesses. Her passion for startups began at Fastcase (now vLex),…