At Menlo Ventures, our investment team likes to get creative with how we catalog companies we encounter in the wild. Much in the way that scientists rely on phenotypes to describe a range of human characteristics (and their mortality rates), this thesis taxonomy allows us to pinpoint qualities that we believe strongly influence outcomes—both good and bad—in the world of fast-growing startups. A company that expresses several favorable traits, not surprisingly, can drive us into an investing feeding frenzy. Those less desirable can make us run for the hills.

This investment index provides us with memorable expressions of our core values. For instance, like sugar addicts, we simply cannot get enough of “layer cake businesses” that have sticky, long-term monetizing relationships with their customers. We also hunt for “beachheads” because of their strong early traction within a niche of a larger market, and may even kill for “flywheels” given their capacity to leverage virality and/or network effects. Likewise, we derive comfort in “buoy businesses” that are structurally capable of floating or generating cash simply via a reduced growth rate. But, we try to avoid “drunken sailors,” “one trick ponies,” “cash-burning machines,” and “craters”—for obvious reasons.

The right combination of characteristics can be multiplicative in impact and create the necessary conditions for capital efficient, exponential—or venture—growth followed by long term, profitable, compounding growth (think: the 20x after IPO). A set of dynamic traits such as these often helps to form the necessary moats that define iconic companies with long half-lives and whose value can last for generations.

For some time, it’s been our thesis that powerful, cloud-native software (SaaS) will disrupt on-premise software and the manual workflows that have defined large parts of our economy. In our hunt for cloud-native vertical and departmental SaaS businesses, we homed in on a SaaS phenotype that gets us very excited: the “trifecta.” For our purposes, the trifecta represents a SaaS product (often only a beachhead) that:

- can stand alone to eliminate, consolidate, or automate busted, manual workflows;

- exists as—or becomes—a system of record and facilitates the data plane; and

- attracts multiple constituents (or counterparties), driving network effects, lateral movement, and monetization within an ecosystem.

Over the past few years at Menlo, we are proud to have invested in a fair share of notable trifecta companies, such as Carta, Qualia, Envoy, Everlaw, Alloy.ai, and Scout RFP. And today, we are delighted to be adding to the portfolio a new trifecta business: Indio.

Our investment in Indio is the outcome of three years of research into insurance tech (insurtech). Before meeting Indio, we had canvassed most of the existing landscape, looking at different lines and different parts of the insurance “stack,” to evaluate opportunities through our “Disruptor vs. Enabler” framework.¹ Nothing really caught our eye. And frankly, given all of the hype around insurtech, we were disappointed to come back empty-handed. Disruptors seemed woefully capital inefficient, and enablers often seemed stuck in long Proofs of Concept with large carriers or were simply dismissed by brokers.

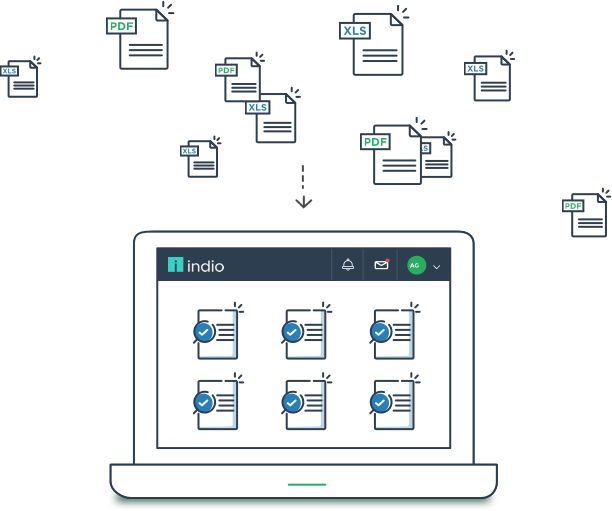

It was, therefore, a relief when we discovered Mike Furlong, Adam Bratt and the rest of the Indio team. We quickly identified Indio as a fast-growing trifecta business—an enabler that is clearly well positioned to catalyze digitization across the property and casualty (P&C) industry. Indio’s beachhead is a white-label software platform that enables P&C brokers to offer a Turbo-Tax-like experience to their end clients and, in turn, run internal operations more efficiently. For being around only two years, the company is off to a smoking start. Indio already has over 250 brokerages (including 30 of the top 100) on its platform and is, for lack of a better term, growing like gang-busters.

How does Indio satisfy the conditions of Menlo’s trifecta? First, the platform obviates manual form filling and data re-entry for both brokers and clients (a busted workflow). Second, client data, which used to sit in PDFs and spreadsheets, now resides in a structured form within Indio (a system of record). This allows the company to create colossal efficiency gain for brokers, especially during renewals. And, finally, the data Indio collects is the data carriers need to make underwriting decisions. Today, they manually re-key data from broker-filled PDFs into their own systems. In the future, they will just connect to Indio.

Safe to say, Menlo’s decision to invest in Indio was a no-brainer. We’re delighted to announce our lead role in the company’s $20 million Series B and look forward to a long and fruitful partnership with the Indio team.

1. In the context of insurance, an example “disruptor” would be a vertically-integrated broker or managing general agent that endeavors to leverage proprietary technology and distribution to win business from existing, traditional players. In contrast, an “enabler” would be a company that sells technology (often in the form of SaaS) to existing brokers to increase tech-enabled efficiency. Each model has its pros and cons. The topic deserves its own blog post.

Tyler is a board partner at Menlo Ventures focused on investing in technology-enabled services and products that are positioned to compound their growth efficiently for a very long time, vis-à-vis sticky long-term relationships with customers and partners. He has coined these businesses “layer cakes” (resulting from customer revenues looking like…