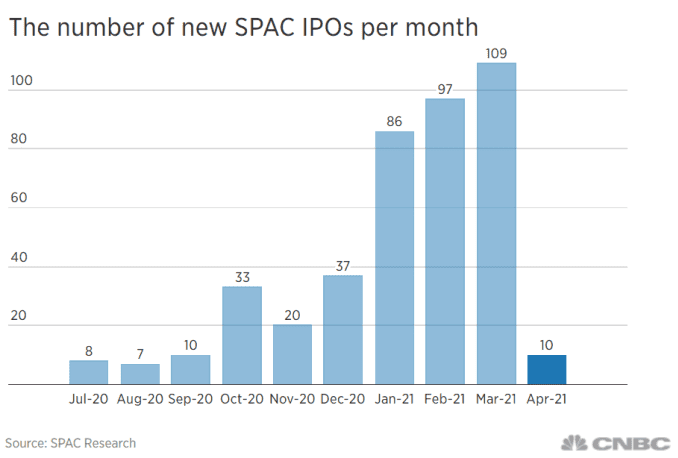

SPACs were seemingly everywhere—a previously esoteric financial strategy exploded into prominence in 2020 and 2021. According to SPAC List, after 33 SPAC IPOs from 2017–2019, 2020 saw 224 SPACs go public, and nearly 300 SPACs listed in the first quarter of 2021.

But then, just as suddenly as they emerged, SPACs faded, with just 10 new IPOs in April. New guidance from the SEC around accounting treatment cooled the market, and gave investors an excuse to pull back from the torrid pace. While SPACs will likely never return to their torrid Q1 pace, they will remain a significant source of financing and provide a much-needed boost to the formation of innovative consumer and “hard-tech” startups.

Mid-last year, I wrote about the runaway train that is venture-backed software companies (both from an exit and financing perspective). Since then, multiples have expanded further, and Zoom, Shopify, and Snowflake have all broken the $100 billion market cap threshold. Given this backdrop, software companies will have no trouble attracting private capital and tapping the public markets at favorable prices through traditional IPOs (or direct listings like Palantir). SPACs have opened up a financing and liquidity source for the rest of the market. This new avenue for growth capital and liquidity will help swing the pendulum toward bolder consumer and hard-tech bets.

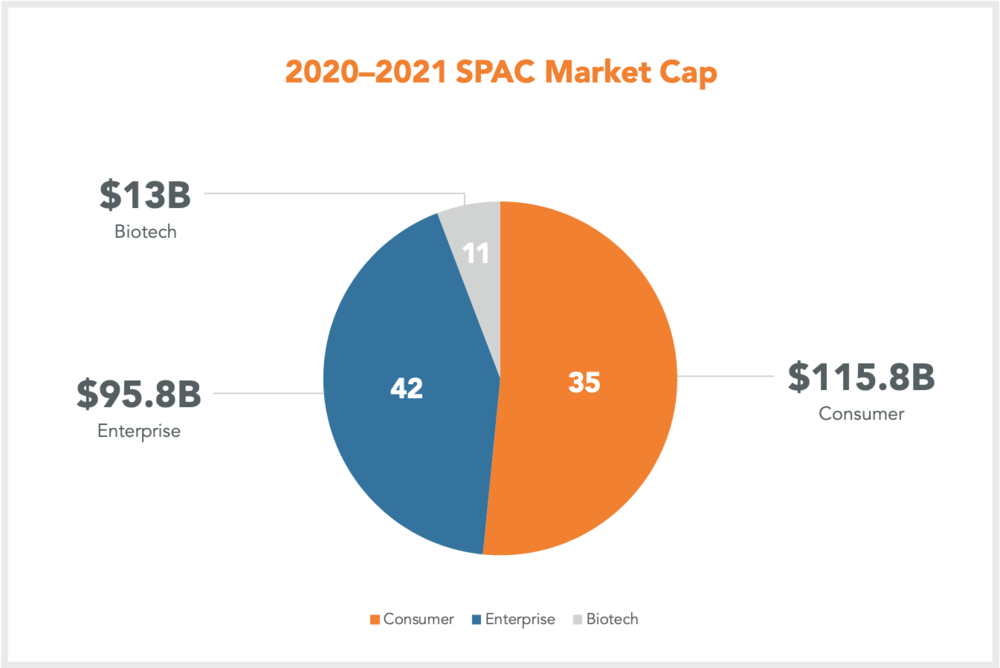

Within the cohort of SPAC mergers in 2020–2021, consumer companies accounted for 52% of the total market cap and were, on average, 45% more valuable than their enterprise counterparts ($3.3 billion to $2.3 billion). Enterprise software companies were almost nowhere to be seen in this crop of companies, accounting for just two SPAC mergers. Compare that to the cohort of 200 U.S. VC-backed IPOs over the same time frame, where 26 enterprise software companies account for $210 billion in market cap.

Many of these consumer companies are highly speculative, and the early selection of SPAC mergers is likely over-indexed toward self-driving, EV, energy, and automotive technologies. However, by showing founders and investors a path to raising capital and liquidity for companies that don’t hit the standard predictability patterns of traditional IPOs, SPACs encourage the entrepreneurial ecosystem toward bolder practices.

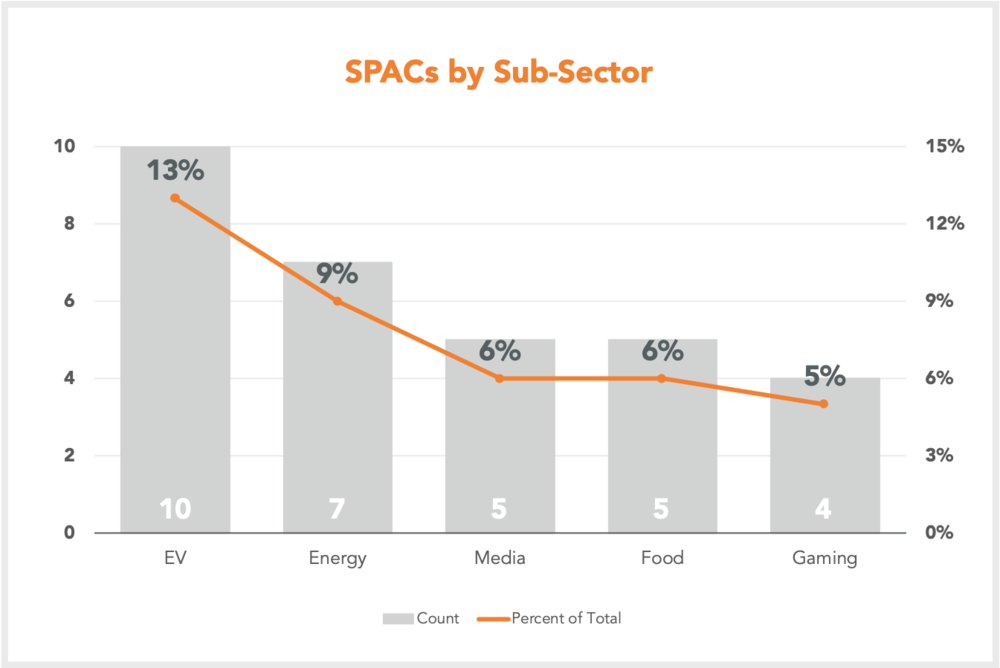

SPACs are also more diverse in the companies that they bring public versus traditional IPOs—while software companies made up 33% of conventional IPOs, EV startups only accounted for 13% of SPACs. The long-tail of sectors represented in SPAC transactions is impressive.

While the current hot sectors in the SPAC world will rotate in the future, they aren’t as concentrated as we might be led to believe. The world of venture capital has become relatively homogenous in its thinking, with lots of money chasing the same few assets. Full-stack funds rapidly consolidated over the last five years, and these funds all target the same set of enterprise software metrics. The SPAC world, while nascent and risky, has the potential to shake up this pattern and encourage the next generation of investments in companies a bit further off the beaten path.

Steve is a partner at Menlo focused on investments in Menlo’s Inflection Fund, which targets fast-growing Series B/C companies. He specializes in AI-powered vertical SaaS investments and supply chain technology, including Enable, Eleos, Observe.AI, Scout, 6 River Systems, ShipBob, CloudTrucks, and Parade. Steve joined the firm in 2015 as an…